Owning construction equipment requires protecting it against risks. If you move equipment from one location to another, risk can shift daily. Whether you own one backhoe or a fleet of excavators, overlooking the fine print in your equipment insurance policy can cost you. These six insurance tips for construction equipment owners will help you avoid the pitfalls and protect your most expensive investments.

1. Audit Coverage for Mobile Use

Not all policies support movement. If your machinery moves to various job sites two to three times per week, verify that your policy accounts for transit, theft, and job-site incidents. Many contractors rely on property insurance when they need inland marine coverage, which is ideal for tools and equipment in transit or off-site. Also, check whether your policy limits apply only to equipment stored at a fixed address.

2. Account for Equipment Downtime

Heavy equipment downtime is expensive. When a loader’s out of service for four days after a lightning strike, you lose time and revenue. Add loss-of-use coverage that kicks in after 72 hours to offset rental costs or missed deadlines. This is particularly important during hurricane season when repair delays stretch from days to weeks due to parts backlogs and technician shortages.

3. Cover High-Tech Attachments Separately

That hydraulic hammer, GPS, or LiDAR scanner might be worth more than the base unit, and it might not be insured. Check if your policy treats tech attachments as separate line items. Most policies only cover the “primary equipment” listed on the schedule. If you’ve added attachments in the last six months, ask your broker to update your declarations page before the next invoice hits your inbox.

4. Understand State and Federal Transport Rules

Crossing state lines in the US is more than a mileage thing. Review the appropriate guidelines for transporting equipment across state lines to avoid gaps in coverage. Improper permitting, axle load violations, or missed inspections can void coverage if an accident occurs in another state.

Before transporting machinery to Alabama or Georgia, for example, confirm that your insurance still applies once you’re outside Florida.

5. Insure Across All Locations

If you operate out of DeLand, Florida but pick up weekend work in Miami, Florida, a policy tied to one ZIP code won’t cut it. Look for insurance that provides multi-site scheduling and recognizes job-site variation. Some policies only apply when the machine is “at home base,” which doesn’t help when it’s parked 180 miles south.

6. Don’t Make Assumptions About Expensive Tools

Protecting your assets is the most essential part of these six insurance tips for construction equipment owners. Never assume a contractor’s liability policy extends to your equipment. If your gear is stolen or damaged while subbing on someone else’s project, the policy likely excludes it.

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

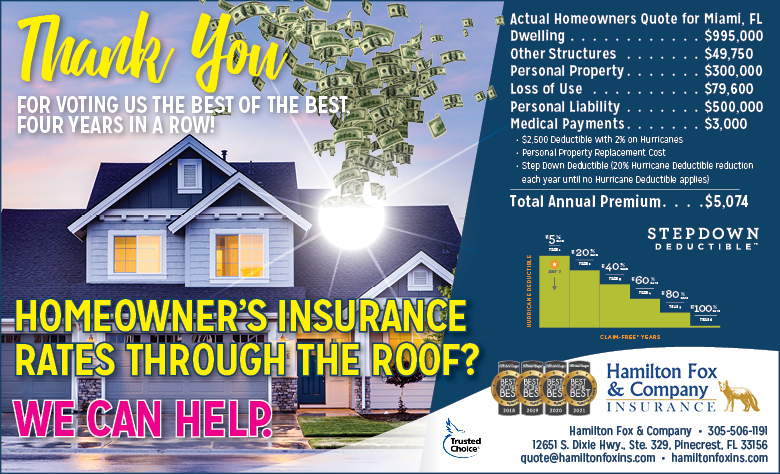

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

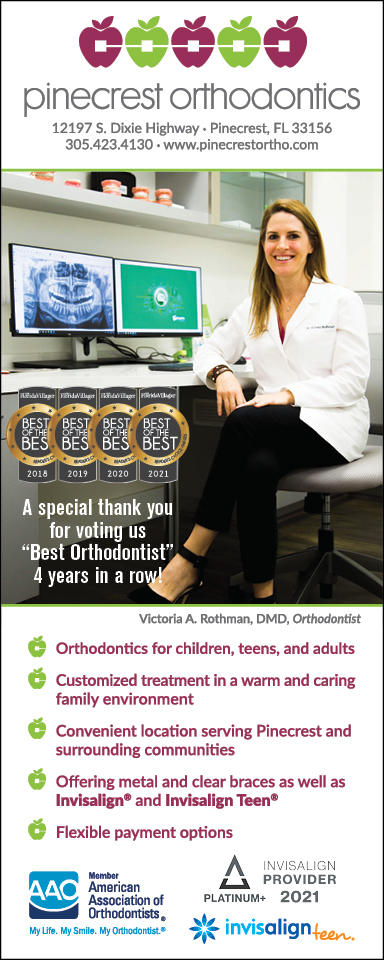

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company