Medicare Advantage is becoming increasingly popular among those who are enrolled in Medicare, with an estimated 31 million enrolled in a Medicare Advantage plan across the United States, or about 54% of all enrollees. With Florida in particular, at 60% of all enrollees.

If you were to read most mainstream media news articles, you might be surprised to hear these numbers. Afterall, most articles portray Medicare Advantage in a very bad light. So why is it that in Florida a supermajority of seniors elect to go with Medicare Advantage for their healthcare coverage?

Is it because Insurance companies are coercing people to sign up? Is the marketing overwhelming? Or could it be that Medicare Advantage just offers better benefits than a Medicare Supplement at a competitive price?

According to David Walls, owner of Florida Medicare Broker, “Medicare Advantage simply offers customers the coverage they are looking for, and at a price they can afford.” In Florida, the typical Medicare Advantage plan offers hospital, medical coverage, and prescription drug coverage – just like you can get with a Medicare Supplement with a Part D Prescription Drug Plan. However, along with it you can often get coverage not offered under a Medicare Supplement. Such as, dental, vision, and even chiropractic care.

Medicare Supplements only cover what Original Medicare [Part A & Part B] covers. It literally supplements Original Medicare. So, if Medicare doesn’t pay anything towards a procedure, neither will the supplement.

Medicare Advantage, however, is privately run by insurance companies. Therefore, the plans have more flexibility to offer more benefits. They must, by law, offer at least the coverage that Original Medicare offers, but are allowed to offer more – and most plan do offer more coverage.

As popularity grows, more people enroll in the plans. 12 years ago, only about 13 million Medicare beneficiaries enrolled in the plans. Today, more than double that are enrolled in a Medicare Advantage plan, and Florida is leading the way with approximately 3 million enrollees. And, as enrollment goes up, more doctors accept the plans, and more benefits come with the plans. The trend does not appear to be slowing either.

Today, it is not unusual to find plans that reimburse Part B premiums, offer over-the-counter benefits, gym memberships, and even rides to the doctor. Dental, vision, and hearing coverage as also become a standard across all plans.

David Walls says that he has “witnessed plans offer richer and richer benefits with every passing year”. Copays continually drop every year, dental and vision benefits become more common, and maximum-out-of-pocket across multiple plans continue to go down. He has worked in the industry for over 13 years and specializes in the Medicare market throughout the state of Florida. He mentions that even though many Medicare Advantage plans offer “all the bells and whistles”, many of his clients still just simply want “flexibility of doctors at an affordable price”. This is why many of his Medicare Advantage clients opt for a PPO.

A PPO allows the customer to see doctors in and out of the network, and without referrals, like an HMO would require. Although the out of pocket costs with a PPO tend to be slightly higher with a PPO, the broader networks seem to appeal to most customers.

As for affordability, most plans do not have a monthly premium in addition to the standard $174.70/mo (estimated to rise to $185/mo in 2025, according to the Medicare Trustees’ Report) Part B premium that commonly comes out of a Medicare beneficiary’s Social Security check. The copay structure on most plans also seems fair in most cases.

The last thing that David Walls stresses, is that customers talk to their brokers about their needs: “Make sure your doctor and hospital of choice accepts the plan that you are choosing, and that your prescription drugs are covered at a reasonable copay, and that you understand how the plan works.”

While most hospitals in Florida accept a wide variety of Medicare Advantage plans, individual doctors can vary significantly in which plans they accept.

Understanding how the plan works is an important detail as well. Unlike Original Medicare, Medicare Advantage will require the occasional prior-authorization for a procedure before its covered. While very common with HMOs, PPOs do not require them as often, statistically about 50% less often than their HMO counterparts. However prior-authorizations are a reality, and can be a nuisance when encountered. David Walls of Florida Medicare Broker reminds us that “While prior authorizations are never a fun experience, this is one the biggest reasons why you should work a local broker. A good broker will be able to get the right people in touch with you much quicker than when working by yourself. The process is almost always faster, and less stressful.”

He also stresses that prior-authorizations should not be a deal breaker for someone looking into Medicare Advantage, as the “horror stories told by some ‘YouTubers’ are most exaggerated to push Medicare Supplements”. When asked why they would do this, David claims “Because they only sell Medicare Supplements due to the extra regulatory burden that comes with offering Medicare Advantage.” He also stressed that he “likes Medicare Supplements, and think they too are a great product.”

Medicare Advantage plans may not be the right choice for everyone, but they may be the right choice for you. It is encouraged that you consider all options when choosing your Medicare plan, and work with a broker that represents several different plans, to be sure you are avoiding any biases.

Lastly, it is important to note that Medicare Advantage plans, like Part D Prescription Drug Plans have one year contracts with Medicare. This means that the plans can, and usually do, change from year to year. For this reason, it is important to check to read the Annual Notice of Change that the insurance company sends out in the early part of Fall to understand the changes coming the next calendar year.

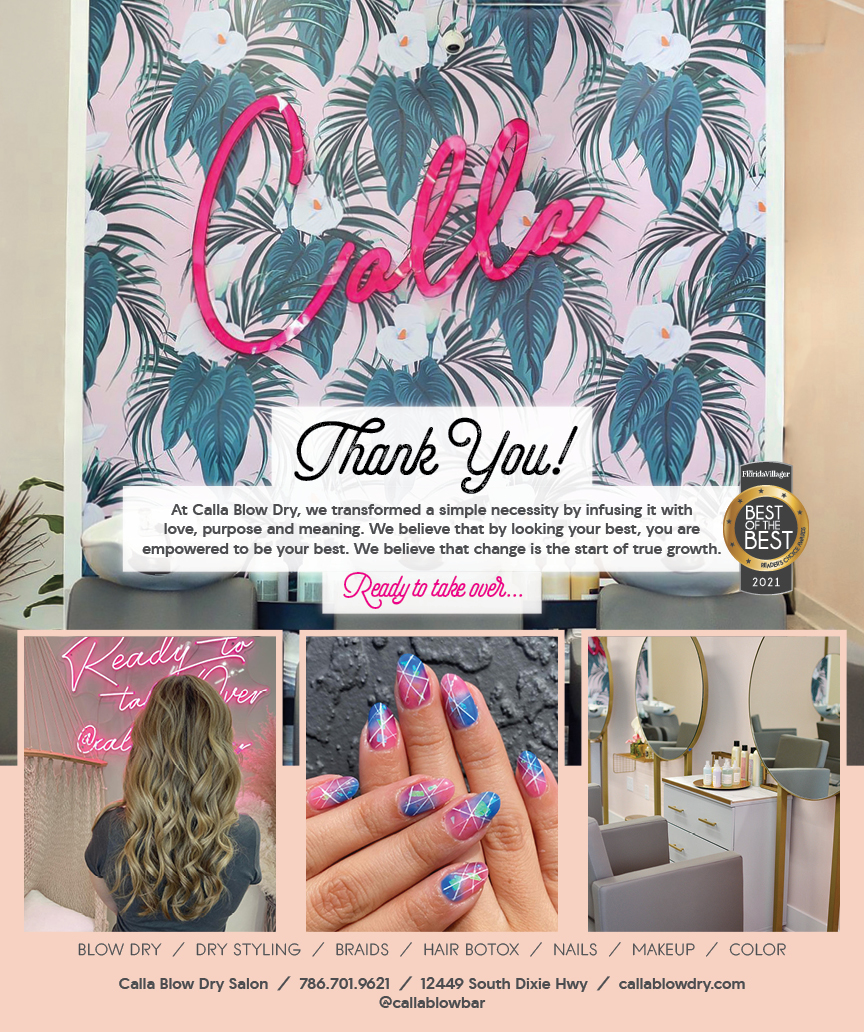

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

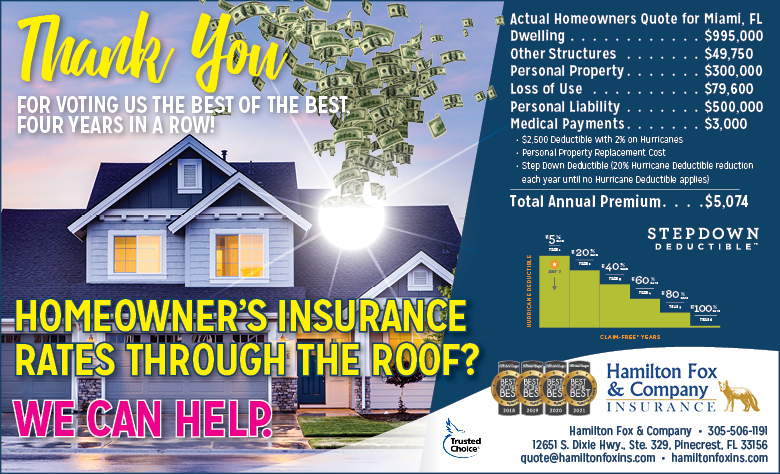

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company