Experiencing a car accident that leads to your vehicle being totaled is stressful and overwhelming. It plunges you into a whirlwind of decisions and actions that could significantly impact your financial standing and future mobility. Here are the most common mistakes you must avoid after totaling your car.

What Does “Totaled” Really Mean?

A car is “totaled” when the cost of repairing it exceeds a certain percentage of its value before the damage occurs, a threshold often set by insurance companies. This percentage varies but typically ranges from 50 to 70 percent. The assessment involves comparing the repair costs against the car’s actual cash value (ACV), which factors in depreciation. In such cases, insurance companies deem it financially impractical to repair the vehicle, opting to pay out the car’s ACV minus any deductible.

Severe flooding or damage compromising the vehicle’s structural integrity can also lead to a car being declared a total loss. If your car isn’t a total loss, replacing the damaged parts with remanufactured components and fixing the entire vehicle is the most practical solution.

Mistake I: Not Understanding Your Insurance Coverage

Comprehensive coverage protects against damage not resulting from collisions, such as theft, vandalism, natural disasters, and encounters with animals. In contrast, collision coverage covers damages from accidents, whether with another vehicle or an immovable object, like a tree or a pole. Knowing which coverage applies to your situation directly impacts the insurance payout you can expect. For instance, if your car is totaled due to a flood (a scenario covered under comprehensive insurance), not having comprehensive coverage means you won’t receive a payout.

Mistake II: Not Completing Payments on Your Totaled Car

Suppose your car is declared a total loss, and the insurance payout does not cover the full amount owed on the loan. In that case, you are still liable for the remaining balance, a situation commonly referred to as being “upside down” on your loan. This discrepancy occurs because the insurance company pays out the car’s ACV, which is the amount you owe. Consequently, if the ACV is less than the loan balance, you must continue making payments until the debt is fully settled, even though you no longer possess the vehicle.

People with gap insurance—policies designed for these exact situations—can avoid out-of-pocket expenses entirely. One advantage of car leasing is that many such agreements include gap insurance policies!

Mistake III: Not Negotiating With Your Insurance Company

Neglecting to negotiate with your insurance company can result in accepting a settlement that may not fully reflect the value of your totaled vehicle. Many car owners are unaware that the initial offer from an insurance company is not final and they can contest it.

Conduct research on the car’s ACV and consider factors like model, age, mileage, and condition to determine how much you are owed. Without engaging in negotiation, you might inadvertently settle for less, which could impact your financial situation, especially when seeking a replacement vehicle.

Totaling your car can be a stressful and confusing experience, but avoiding these common mistakes can help you navigate the aftermath. Trust in the process, and remember that each step you take moves you closer to resolving the situation.

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

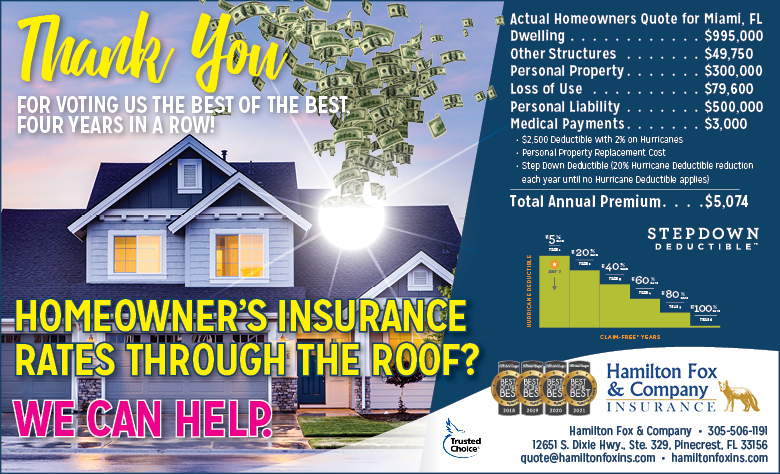

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company