If you’re concerned about getting the best health care as you age, you may want to consider Medicare. Medicare is a health insurance program provided by the government that is designed for individuals who are age 65 and over. Medicare is also for disabled individuals who are younger than 65 and for individuals with chronic illnesses such as End-Stage Renal Disease, which is permanent kidney failure that requires a transplant or long-term dialysis.

Here are some additional things you should know about Medicare so you can apply for yourself for a loved ones to ensure you receive the medical care you need.

Parts of Medicare

There are a few main parts of Medicare that will cover detailed medical services:

- Part A of Medicare is for hospital insurance. This covers your hospital stays, home health care, as well as medical care you’d receive in a nursing home or facility. Part A also covers hospice care.

- Part B is medical insurance which covers outpatient care, preventative services, medical supplies that you may have to use at home, and services from specialty doctors.

- Medicare does cover cancer treatments for people that are over 76. Your cancer coverage will work differently depending on if you’re in the hospital or an outpatient facility.

- Medicare Part D is coverage for prescription medications. This part of Medicare helps cover the costs of any medicines prescribed by your doctor as well as vaccines or recommended shots.

How Original Medicare Works

Original Medicare will cover most of the cost for necessary health care supplies snd services. Once you meet the deductible, you’ll pay your portion for services and supplies as you receive them. There’s no out-of-pocket limit for the year unless you have another form of health insurance such as Medicaid, Medigap, or coverage from your employer or union.

The services Medicare covers have to be medical necessities. Medicare will take care of certain preventative services as well such as health screenings or shots. If you go to a physician or other health care provider that accepts the amount approved by Medicare, you may have to pay less out-of-pocket costs. However, you’ll have the pay the total cost for services if Medicare doesn’t cover the specific service you’ve received.

Benefits of Original Medicare

If you have original Medicare, you can visit any physician in the US that accepts Medicare. You’ll also be able to join a separate Medicare drug plan to get coverage for your prescriptions. With Medicare, you can also buy Medigap to lower your share of the costs of medical services.

You must be in the US legally to apply for Medicare and receive Part A and Part B coverage. Medicare will not allow enrollment into its drug plan or Advantage plan if you are not legally present in the US.

Medicare Advantage

Medicare Advantage plans combine your Part A, B, and D coverage into a single plan. You’ll also receive some benefits that are not offered with original Medicare such as dental, hearing, and vision services.

With Medicare Advantage, you’ll join a healthcare plan that is offered by private companies approve by Medicare. The companies must follow Medicare-mandated rules and each of the plans will entail different rules for the services you can receive, including referrals to specialists. The monthly premiums and costs you are responsible for will vary depending on the Medicare Advantage plan you select. Your plan must cover emergency care, urgent care, and all services that are medically necessary and covered under original Medicare. Some Medicare Advantage plans will provide additional benefits to treat specific health conditions.

Medicare Advantage allows you to use in-network doctors for routine and urgent care. You may be required to pay a premium along with your Part B premium. Some plans have a $0 premium and some are designed to help you pay all or a portion of your Part B premiums.

How Medicare Works with Other Types of Insurance

If you have Medicare along with another type of health insurance from Medicaid, your employer, or coverage you obtained after retirement, each of your policies is known as a “payer.” If you have several payers, you’ll need be aware of the “coordination of benefits” rule to determine who will pay first. Your primary payer pays if this is the insurer that owes the cost of coverage first. The rest is sent to the secondary payer or to a third payer if necessary.

Your primary payer will pay up to the limits of the policy coverage. Secondary and third payers will pay the remaining balance if the primary payer didn’t cover the total cost of your medical care. If your secondary payer is Medicare, this payer may not cover all the outstanding costs. If you have a group health plan or receive healthcare coverage as a retiree, it may be best to enroll in Part B Medicare to make sure your services are covered.

If your insurance company doesn’t pay your insurance claim within 120 days, your physician or specialist will likely send a bill to Medicare. If this happens, Medicare will likely make a payment and then recover any payments that were originally the responsibility of the primary payer.

Here are some important things you should know about Medicare before you enroll. These details will help you customize your coverage according to your health needs.

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

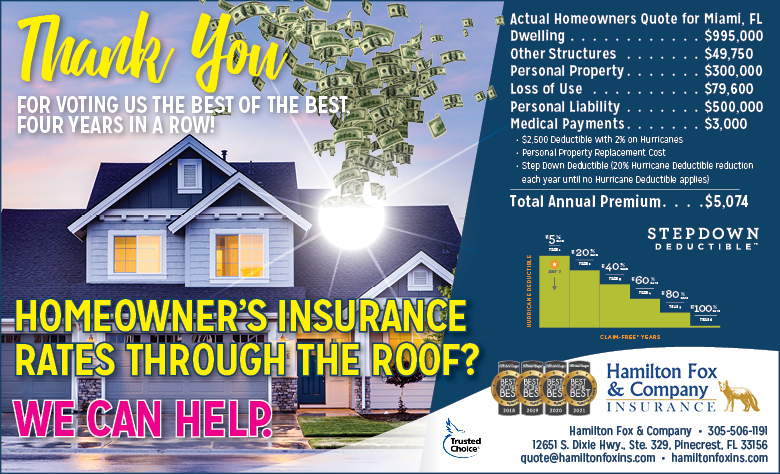

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company