If you have owned your home for more than a year, you have probably realized its value has increased substantially and the idea of selling your home to cash in on that increased value has most certainly crossed your mind. In fact, it’s crossed your mind that much that you’ve decided to look into “we buy houses Vancouver WA, California, and Florida” services to get it done as soon as possible. Not only that, but you have gone online to check the automated “estimate” of your home. You would have also called your trusted real estate advisor to get a (better, more accurate) valuation on your home. You might have also checked the living costs in your area by looking into websites like https://tracyhomesales.com/tracy-ca-cost-of-living, or elsewhere. And what a nice surprise that was! You have a large amount of equity built-in, so you say, “Let’s sell it and move!” But should you sell or buy first?

Allow me to show you a few possible scenarios so you can decide how to go about selling and moving in a way that fits your financial situation and your family best.

You’ve got the cash and don’t want to be rushed

If you have the funds readily available for a down payment or to pay for the new house in full, you can buy your next home before selling the current one. In fact, buying before selling allows you to go home shopping with less pressure. You can take your time to find the right home, close on it, move in, and then list your previous home for sale, which might be really helpful if you were relocating much further, such as moving from Florida to Las Vegas and you have already found your new home using websites like https://vegashomesnv.com. However, if you will be financing the purchase, check with your lender to ensure you can carry both properties’ costs for the period of time estimated to sell your first home.

Cash for the purchase is tied to your current home

If you are like most homeowners, your home is the largest asset you own; and you might need the equity built into your home to pay for the next one. In this case, selling your current home first is the evident solution – yet not the only one (more on that later). There are a few ways to go about doing this:

Contingent to sale of buyers’ home

After putting your house in the market and receiving an agreeable offer, you can make an offer on a home to purchase contingent upon the sale of your current home. This contingency ties both transactions in a way, and if your home sale were to fail within the stipulated time frame, you can walk out of the purchase without penalty. Current market conditions in our area make this strategy challenging, as this added contingency decreases your offer’s competitiveness in the eyes of the sellers. They can most likely get other potential buyers to make good offers with less strings attached.

Post Occupancy requirement

A more realistic alternative for this seller’s market is to request a post-occupancy period as a condition on the sale of your current home. This allows you to close on the sale of your home and collect the proceeds but remain living in the sold home for a few more weeks. With money in your pocket, you can put a strong offer on your next home.

Temporary housing

If a post-occupancy is not an option on the offer you accept to sell your property, you will need to find a temporary home for your family from the day of closing on your former home until you complete the purchase on the new one. A short-term rental of a furnished place, moving in with relatives or renting an unfurnished home for a full year are some of the viable options. Your family situation and budget will determine the best course of action.

Other alternatives

There are some additional options with added complexity and creativity that allow you to get the cash out of your current home to purchase the new one without selling first. Tapping into your home’s equity by way of a home equity line of credit – or even a refinance with cash out – could be an option for you. Check your particular situation with your preferred lender.

For a more personalized assessment of your options, contact a trusted real estate advisor.

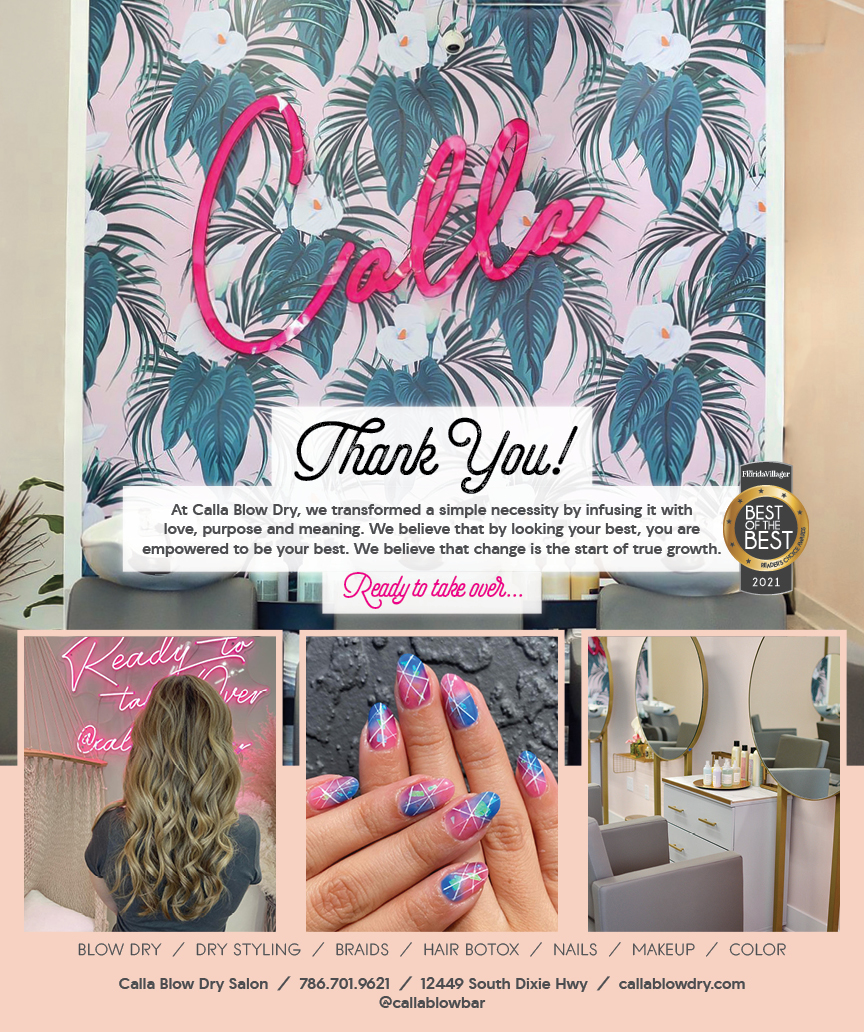

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

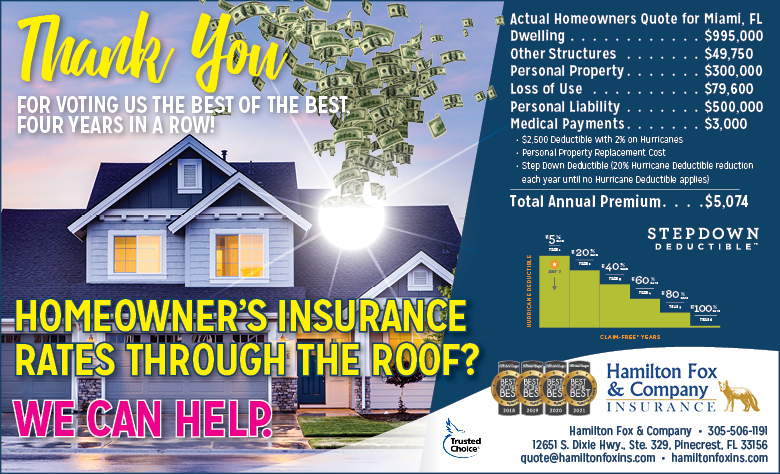

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company