If you are a parent, whether your child was just born or about to finish high school, you’ve probably wondered how you are going to pay for college. According to the U.S. Census Bureau, in Miami-Dade, Broward and Palm Beach counties, there were over 5.5 million children under the age of 18 in 2010. Since then, estimates on average are that those counties grew by about 13.3 percent, which translates to well over six million kids who are potential candidates for planning.

But how do families go about paying for college? With the cost of college rising faster than inflation, it is important to begin the planning process early. According to the 2016 Sallie Mae report, “How America Pays for College,” scholarships and grants paid 34 percent of college costs, loans to both the student and their parents made up 20 percent, but the remaining 46 percent came from family income and savings.

Even for wealthier families, covering the exceptionally high cost of higher education can seem daunting, particularly if you have more than one kid bound for college. That’s why it is important to involve the entire family in college planning-and act early, whether it be looking at investment options via SoFi or considering longer-term saving goals.

Before your family prioritizes saving for college, it is important to first eliminate debt that is draining monthly cash flow and eating into your returns. This may seem overwhelming, but devising a strategy to tackle the highest-cost debt first will help you work your way down. Tackling your debt is the first step in financial planning, especially if you’re looking into Walker CPG retirement planning or other similar options. There is so much that you will need to address while planning for your golden years. You will need to ensure that your retirement plan is up to date, estate planning and finances are dealt with, and a corporate trustee is selected. While it is great to have your child’s future in the forefront of your mind, it is also important that you think about your future as well.

It is also a good idea to include all family members who will contribute to college savings in the process. This may include aunts, uncles, grandparents-and yes, even the kids. When they are old enough to grasp the concept, involve your children in the conversation. If they’re expected to contribute toward college expenses, a good time to talk with them may be when they’re in high school and beginning to think about college.

Why this is important is that a record 2.8 million Americans over the age of 60 had outstanding student loans as of 2015. Close to 40 percent of federal student loan borrowers age 65 and up are in default, which is the highest rate for any age group.1

Putting your child’s well-being above your own is a noble and understandable tendency among parents. But it is never advisable to sacrifice your own savings to put a child through school.

One issue is that private student loans do not have the same protections that federal student loans do, such as income-driven repayment plans and forgiveness options.

“Getting a college degree is important for your children’s success. It’s important to remember that despite the high up-front cost, college degrees are worth it over the long run in terms of lower unemployment rates and higher earnings,” says Justin Waring, an Investment Strategist at UBS. “But as the parent, you’re not directly reaping those benefits, and you have much less time than your children to recoup the cost of college.”

Before you decide how much you’re going to contribute toward your child’s college education, make sure that you work with Financial Advisors to build a financial plan to help you stay on track to meet all your retirement goals.

Planning for the rising cost of college is much easier when it is a family affair. However, if you have questions or run into challenges, it is a good idea to bring a financial advisor on board to help you understand your options and to provide sound, practical guidance.

1.”Student Debt Now Affects a Staggering Number of Elderly Americans,” chicagotribune.com/business/ct-student-debt-elderly-americans-20170116-story.html.

Carlos Lowell is senior vice president of wealth management and financial advisor for The Lowell Group at UBS Financial Services Inc. in Coral Gables, Florida. He and his team work with an exclusive group of individuals and families providing one-on-one comprehensive financial solutions. Focusing on business growth and succession planning, he brings an in-depth knowledge of risk management, financial planning and business valuation planning to clients, from entrepreneurs to athletes to medical professionals, in order to customize and implement comprehensive financial strategies. He can be reached at carlos.lowell@ubs.com.

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

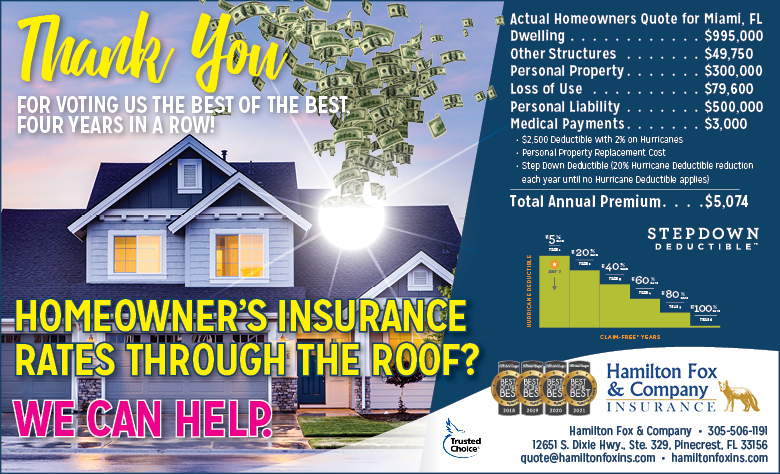

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company