With hurricane season upon us, many South Floridians are taking a closer look at an important aspect of hurricane prep: their insurance coverage. As a longtime insurance professional (a third generation agent, it literally runs in his family), Hamilton Jones is about as knowledgeable as you can get, regularly working with clients to ensure (no pun intended) the best and smartest coverage for each individual situation. “As an independent agent, we can secure alternative coverage terms from multiple insurance companies very easily and seamlessly for our valued clients,” says Jones. We spoke with Jones as the season kicked off to learn more about coverage concerns, when to check in and the unique challenges of owning a home in Miami.

Miami is an extremely unique city when it comes to insurance needs, how does that manifest in working with clients?

Miami and the surrounding areas are truly a wonderful place to live, however, living in paradise comes at a hefty price. South Florida has the highest home insurance costs and has one of the Top 10 most expensive auto insurance costs in the nation. Because we are a coastal city, flood insurance can be a huge expense as well and can vary greatly from home to home. Plus, Miami residents love having toys, such as boats, which can present their own challenges when it comes to insuring them. Our clients expect more than a simple product or policy; we become their trusted insurance advisor.

What are three things Miami residents should consider when it comes to insurance that most do not?

- Consider purchasing an Umbrella policy; South Florida is an extremely litigious area.

- Don’t exclude uninsured/underinsured motorists coverage on your auto insurance policies. This coverage may be viewed as somewhat pricey but it is well worth it. If you have any previously convicted drivers on your insurance, it may raise it up quite high, so finding bespoke specialist insurance schemes will be of great help and you can see how that will fit in with your other policies.

- Look closely at the personal property that needs to be insured within your home. The Homeowners policy form provides very limited coverage for jewelry, art work, firearms, collectables and other fine objects. These items should be individually scheduled on your policy..

What is the number one question/concern you hear from clients regarding hurricanes and what is your advice to them?

Surprisingly we hear comments like “Citizens [Property Insurance Corp.] is my only hurricane insurance option because of where I live” or “It’s too late to buy hurricane coverage now because we are in hurricane season.” Fortunately, these comments are not true. We offer Citizens alternatives that, in most cases, provide pricing relief and we are actively selling new windstorm insurance policies throughout hurricane season. The only time we can’t offer windstorm coverage is when there is a tropical storm or hurricane in close proximity of Florida.

You have a great and informative blog on your website. How important is it for clients to educate themselves and understand their policies?

Thanks! It is very important for homeowners to take ownership when it comes to protecting their property and themselves. Informed homeowners make the best clients because they ask the proper questions. This allows our agents to offer a more appropriate insurance solution.

How often do you advise clients to revisit their policies and adjust?

It really depends on the situation. If you are currently insured with Citizens or through the secondary market (excess and surplus lines), I would recommend every year; the same if you make a substantial improvement (new roof, all new plumbing/pipes, etc.) to your home. If you are insured with a standard company and you feel that you have a competitive product, then every two-to-three years.

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

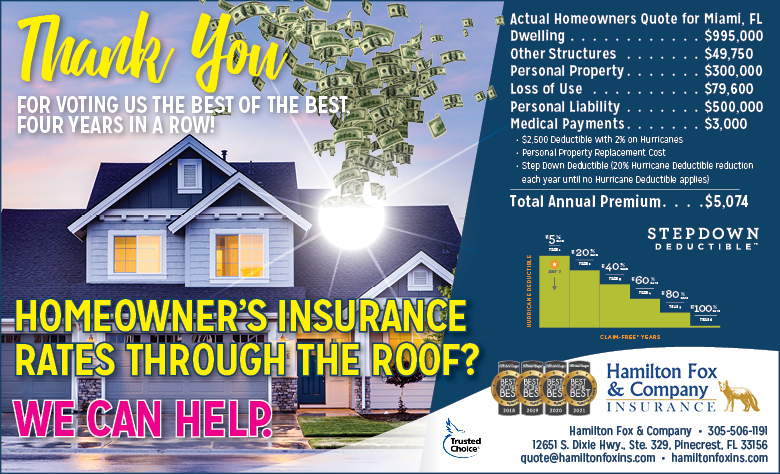

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company