Valentine’s Day is quickly approaching, which means that couples are likely to propose to their significant others. But before couples say “I do,” there are some financial questions they should consider. This conversation can help ease potential conflicts over finances, which according to a survey by Money magazine, is cited as the top source of stress in 35percent of relationships.

Bank of America offers this checklist for any future newlyweds to consider:

Catalogue what you’ll bring to the marriage

- If you’re both employed, two salaries can be a considerable benefit toward building your long-term financial future. Discuss your combined cash, savings and investments.

- Make sure that all of your financial bases are covered by reviewing all credit cards and installment debt.

- Does either of you have student loans outstanding?

- What are your real estate assets and mortgage liabilities?

- How about automobiles, along with the liabilities for their loans, leases and insurance?

- Personal possessions such as family heirlooms, jewelry, fine art and antiques?

Chart your immediate course together

- Have you considered a prenuptial agreement? This is a legal document that permits a couple to keep their finances separate and to determine control of property and assets either partner might have had prior to the marriage. You can learn more about the importance of prenuptial agreements by reaching out to a team of prenup lawyers in your area.

- If either of you has children or other dependents, how will you address their financial interests in the new family?

- Have an honest conversation about financial habits and objectives. Will you have joint or separate checking and credit accounts? Who will ensure the bills are paid each month? How will you set family budget and spending priorities?

- Determine whose employer-sponsored health insurance offers more attractive benefits.

Discuss your long-term joint financial goals (buying a home, retirement, etc.)

- How much will each of you contribute to your employer-sponsored retirement savings plans?

- Will you need additional retirement resources such as an IRA or annuity?

- Did you create a savings plan to accumulate the down payment needed to finance a home purchase?

- Have you identified other financial goals that might need a sustained savings program, such as starting a business or acquiring a second home?

Budget for your wedding and honeymoon

- Determine how much you want to spend for the ceremony, celebration and honeymoon trip.

- Decide who you want to invite to your wedding and to participate in the wedding party.

- Identify potential locations and costs for the celebration. Some people choose to elope to Gatlinburg and other places instead of having a big wedding so that they can go on an even better honeymoon. It just depends on what you value as a couple.

- Consider all cost factors of the trip itself, including transportation, lodging and meals.

Getting married or moving in together can be the start of an exciting new adventure. This transition can be made even more smooth through open communication and smart planning.

(Visited 35 times, 1 visits today)

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

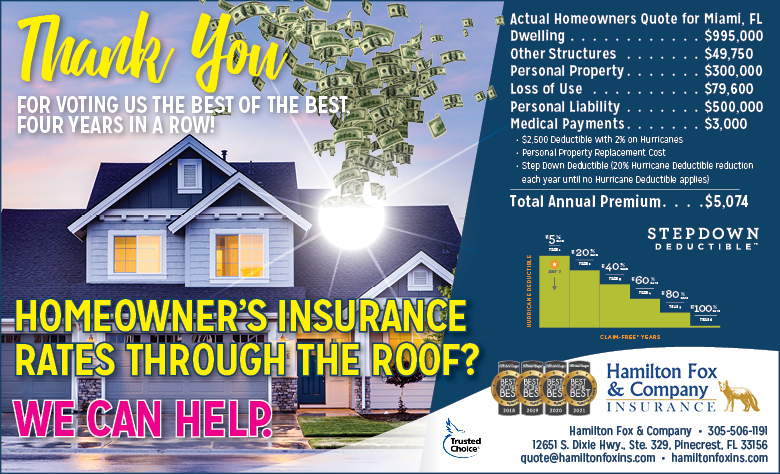

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company