Despite Florida’s booming housing market, many homeowners continue to struggle to pay their mortgages, faced with either financial distress, unemployment or other COVID-related issues. While COVID-related programs offered by the government have ended, mortgage modifications are still around and may be the difference between keeping your home or losing it in foreclosure.

What Is a Loan Modification?

A mortgage loan modification is an adjustment to any term of your current existing mortgage. It could be an adjustment of the interest rate to a lower one. It could also be an extension of the loan lifetime, extending a 30-year mortgage to a 40-year mortgage, to lower the monthly payments. It could also mean a forgiveness of a portion of the mortgage balance, or simply adding any past due amounts from months or years of nonpayment to the back of the loan. All these adjustments are done for the homeowner to be able to keep their home and afford their payment.

A loan modification is not a refinance. Refinancing a mortgage means ending your current mortgage and taking out a new loan. This often involves an appraisal and credit checks as well as closing costs.

Rather, a loan modification changes the terms of your existing mortgage while the original mortgage remains in place. There are no closing costs or out-of-pocket costs to the homeowner associated with the modification.

Why Do Lenders Agree to Modify Existing Mortgages?

Most lenders prefer to keep the current homeowner in the property rather than initiate a foreclosure. Foreclosures are not only expensive for the lender but take years to process through the court, resulting in significant losses for the banks.

Is It Easy to Qualify for a Loan Modification?

Banks apply formulas to determine whether the borrower qualifies for a loan modification. This includes determining the current property value, as well as debt, income and credit standing. Many attorneys, such as my firm, who have been assisting borrowers with loan modifications since 2008, have programs that make the same calculations the banks do in order to qualify our clients. With these programs, we can prequalify clients prior to applying for a loan modification and present the most viable solutions to each homeowner in distress.

Will Your Lender Agree to Modify?

A lender will not agree to modify your loan merely because you are able to prove financial hardship or COVID-related hardship. You will also need to show that you have the resources available to make the payments in the future. It takes an experienced negotiator to review all your qualifications and then submit the proper package to your lender.

Hiring the right lawyer to handle your loan modification can make the difference between an approved modification and foreclosure. While we have been handling all types of loan modifications, foreclosure defense, refinances and all other mortgage-related matters for over 23 years, the key is to make sure you qualify for the program you want prior to submitting any application.

Feel free to contact me to discuss your loan options. Whether you are looking to modify your loan or refinance, are facing foreclosure or merely want to strategize to determine what your best options are for an investment property, we are here to help. Contact us today for a free consultation. It could be the difference between keeping your home or losing it.

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

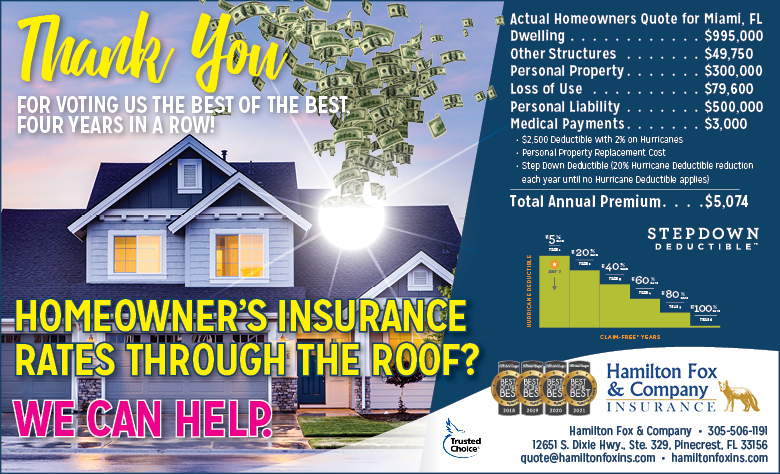

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company