Would you believe me if I told you that in early April the Ways and Means Committee of the U.S. Congress passed a bill with Unanimous Bipartisan support?! Well, it did. It is paired with a similar bill in the Senate, the Retirement Enhancement and Savings (RESA) Act of 2019, giving it a decent chance of becoming law. And you thought our elected officials weren’t getting anything done!

The SECURE (Setting Every Community Up for Retirement Enhancement) Act seeks to take steps toward enhancing the available tax breaks for retirement savers as well as encouraging more people to participate. Concurrently, the RESA bill’s main purpose is to provide multiple employer retirement plans (MEPs) to reduce the cost of providing retirement plans to employees at small businesses by allowing two or more unrelated employers to join a pooled employer plan (PEP). It is estimated that this provision will result in the formation of 600,000 to 700,000 new retirement accounts.

Both bills include a revenue-raising measure (read: more tax) that would curb the tax deferral benefits of “stretch” IRAs which is the main point I’d like to review since it could affect many of you who own or will someday inherit a retirement account(s).

Under current law, a beneficiary who inherits an IRA or 401K account upon the death of the account owner can choose to take payments over their expected lifetimes with amounts remaining in the retirement account continuing to accumulate tax-deferred. This is the ability to ‘stretch’ the inherited retirement assets and spread the withdrawals, reducing the beneficiary’s tax exposure.

The RESA bill would limit these “stretches” to aggregate account values under $450,000. Any amount over this must be distributed within five years of the death of the account owner (there are certain exclusions). The SECURE Act is slightly different. It has no minimum account value but would limit payout to 10 years. The legislation also makes it easier for employers to offer annuities in 401(k) and 403(b) retirement plans. (Read: heavy lobbying by insurance companies that sell these annuities). This will allow for lifetime income stream options. Other important changes include:

Raising the age for required minimum distributions, known as RMDs, from investment accounts to 72 years of age from 70 1/2 years. Americans are living longer and shouldn’t be forced to take money out of the markets just because of their age.

- The bill also requires retirement plans to open up to all employees who either work 1,000 hours in one year or at least 500 hours for three consecutive years (under current law, employers could set any eligibility rules they wanted, as long as employees who complete 1,000 hours of work in one year can enroll).

- The SECURE Act also allows employees to invest up to 15 percent, up from 10 percent, of paychecks to their 401(k) plan.

- Increasing the tax credits provided to small businesses who start up retirement savings plans and/or include automatic enrollment.

- Americans can take out money from retirement accounts without a penalty for a birth or adoption, up to $5,000.

- One provision not related to retirement — the SECURE Act would expand 529 college savings plans to cover the costs of apprenticeship programs and homeschooling. And here’s the best part: It allows 529 funds to be used to pay student loans up to $10,000.

It’s about time our lawmakers address a very important weakness that exists for our country’s aging demographic – helping individuals be self-sufficient during their golden years.

Wealth Engage is located at 9155 S Dadeland Blvd Suite 1014, Miami, FL 33156. For more information, please visit WealthEngage.com. You can also reach Gus directly at 786-315-4870 or gus@wealthengage.com

Securities offered through Raymond James Financial Services, Inc., member FINRA / SIPC. Investment advisory services offered through Raymond James Financial Services Advisors, Inc. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk. Any opinions are those of the author and not necessarily those of Raymond James. The website link included is provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any third-party web site or their respective sponsors. Raymond James is not responsible for the content of any web site or the collection or use of information regarding any web site’s users and/or members.

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

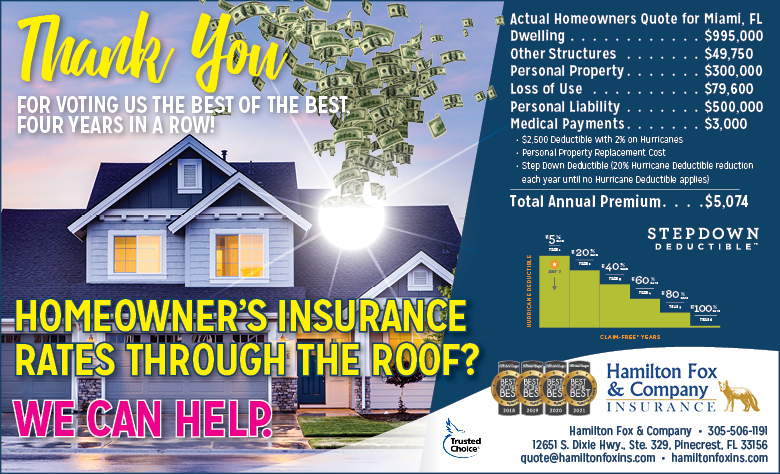

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company