Most people are under the assumption that a flood only happens during a tropical storm or a hurricane. New buyers of property sigh with relief when they hear their property is in the “X” zone on the flood map and not required for closing. What most people fail to realize is that your homeowners insurance does not cover flood and a flood event can hit at any moment.

Tropical Storm Imelda was a mild tropical storm that hit the Texas coast on September 17, 2019 as a minor weather event, but caused 43 inches of rain. The national Flood Insurance Program (NFIP) paid out $738 million on 11,000 claims. According to an NFIP spokesman, that is close to the amount paid on 16,000 claims from Hurricane Florence, a category 1 Storm that hit the coast of North Carolina in September of 2018.

The numbers are staggering. In 2019, a relatively quite year for flooding, the NFIP still paid out $1.47 billion on 35,000 claims. As early as June of 2020, the NFIP received 3,143 claims with a payout to policyholders of close to $44 million.

Of the more than 200,000 homes that were damaged during Hurricane Harvey, three-quarters did not have flood coverage, leaving people waiting on help from the Red Cross or abandoning their homes completely. Although, again, it doesn’t always take a named storm to cause a flood.

Heavy rains, dam failures, excessive property development like we are seeing in South Florida, and even construction projects change the water drainage routes that can result in widespread flooding.

“We’ve altered the landscape of mother nature. Whether it is a commercial project, marine boats moored in the marina, nothing creates more damage and property loss than flood,” states Maria Lemorane, a conservationist with The Save Miami Project.

No matter what property you own, flood is not covered under any homeowners or commercial policy except for rare exceptions on some commercial policies. This is something that commercial property managers may need to keep in mind when they carry out a soc audit. A flood is recognized as standing water or water that infiltrated a home or building and 1,000 feet around that property. Flood does not cover broken pipes within a building, leakage or other mechanical issues within a structure.

There are several types of Flood Insurance available at affordable rates through several different companies that must cohere to the standards put in place by the NFIP. There are programs that offer residential coverage in the amount of $250,000 for the building and up to $100,000 for the contents. For commercial or non-residential structures, the max amount is $500,000 for the building and $500,000 for the contents. A condominium association can purchase a policy for all the common areas of the building, but each unit owner will be responsible to insure their own contents. Many companies offer excess flood for large structures where the max that the NFIP program offers does not adequately cover their risk.

The rise of private flood companies offering better terms and higher limits means that the cost to the consumer is even less for this valuable protection.

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

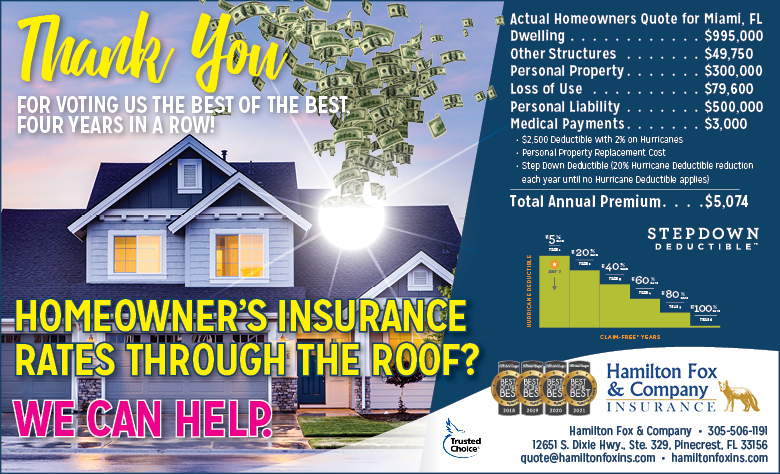

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company