September is traditionally the month when most students return to school and the hustle and bustle of homework and after-school activities begins. If you are the parent of a high schooler, however, this is also the time when you are focusing on selecting a college—and how you are going to pay for it.

While many people think that paying for college is primarily a concern for lower- and middle-class families, I can tell you this also affects affluent parents. The cost of attending college has skyrocketed since I went in the 90s. According to the organization College Board, the average annual cost of college is $20,000 for an in-state public university or $47,000 for a private university. Keep in mind, this is an average, some of the highly ranked schools can cost in excess of $70,000. Since these are “per year” figures, you could spend anywhere from $80,000 to $280,000 for four years.

This is where my husband and I were two years ago when our eldest daughter, Madison, was a senior in high school. It was nerve-racking as we negotiated the maze of college admissions. While we had great college counselors to help us, we were the ones left to navigate the finances. We were fortunate to have grandparents who provided some college savings, yet, we still had many things to figure out. Here are some of the things that we learned along the way.

Remember what happens when we assume:

I strongly suggest that people approach the college admissions process without any preconceived notions. First, familiarize yourself with “net-price calculators.” These can be found on many school websites as well as on College Board’s website. It is important to have an idea of what the cost will be, but remember, this may not be what you end up paying. Next, do not assume that financial aid or a scholarship will or will not be given. I strongly recommend that everyone fill out a FAFSA form and submit it as early as possible. This is the form that most colleges rely on when assigning need-based aid and other funds such as work study and grants. Once colleges receive this, they can establish what your admitted child’s expected family contribution will be and then can develop an aid package. Having this information early will allow you time to review different packages and possibly negotiate a better one.

You expect me to contribute how much?!

When we went through the college admissions’ process, we discovered a brand-new acronym, “EFC” or Expected Family Contribution. This is the amount of funds that you as a parent are expected to contribute toward your child’s college education. The amount is determined by forms like the FAFSA or CSS profile. Evaluators will take into consideration such things as your adjusted gross income, age, and number of children attending college. Parents should familiarize themselves with the College Board EFC Calculator. If you can get an estimate of what your EFC will be, you can determine if you will be a candidate for need-based aid. In the event your estimate is high and your child will not qualify for financial aid, your child can start concentrating on apply for merit aid and private scholarships.

The Finish Line

When we started this process, we looked for an institution that would allow our child to blossom and receive the education she needed in order to reach her goals. With this in mind, we were considered how long it took the average student to graduate and what their employment prospects would look like after they finished. These figures helped us evaluate what the picture would look like for our daughter after graduation. It is also crucial for you to know how many years on average you will be paying for tuition and what the financial picture will look like for your child when they graduate.

I cannot begin to describe the emotions we felt as we started the college search process with Madison. We discovered that while we had thought of college planning as a part of our overall financial plan, when the time came to look at schools, apply and then decide on where she would go, we found ourselves navigating through a maze.

The tools and tips highlighted here are designed to help empower you during this process and to take away some of the stress and uncertainty we faced as parents.

Victoria Lowell is a financial educator dedicated to empowering women with the knowledge to become active participants in the planning of their financial future and well-being. As a Certified Divorce Financial Analyst® (CDFA®) and former financial advisor for UBS Financial Services, she recognized a need to help women assert themselves fiscally. Lowell recently launched EMPOWERED WORTH™, a resource for financial coaching geared toward educating women and giving them the tools to not only meet their immediate economic needs but to attain long-term goals

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

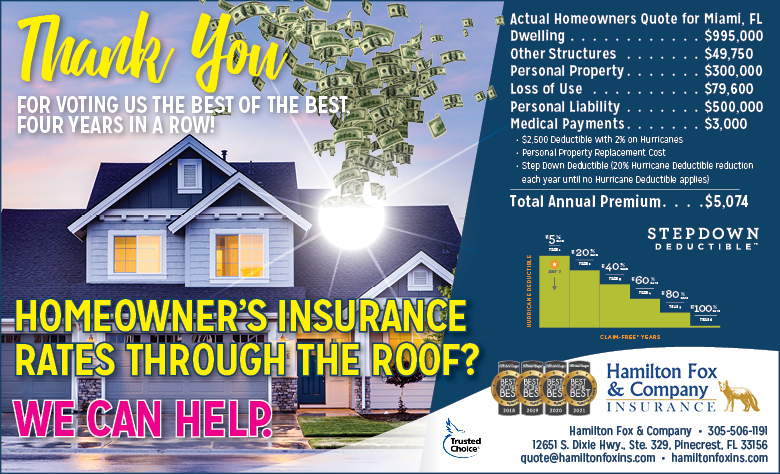

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company