We all know that a new hurricane season begins each year on June first. Last year’s season was a good reminder that some of us were not as prepared as we initially thought. Although we were spared “the big one” with Hurricane Irma, many of us found ourselves re-evaluating our preparedness for a storm while others are still waiting on homeowner’s insurance claims to be processed. This year, it’s a good idea to be ready ahead of time, especially when it comes to ensuring your home and belongings are protected if we get another major storm. It is why it is worthwhile to speak to someone like State Farm Insurance about the options available when taking out said insurance. Unfortunately for us, we don’t know when a storm will happen in our area, so having the best home insurance already in place will be one less thing to worry about if it does. By deciding to look into companies like BST Insurance Brokers Ltd, and the article they wrote about home insurance, you will be able to find out everything you need to know about the different types of policies, and which one can offer the relevant protection in case of a storm. You may not realize it now, but it could be one of the best things that you decide to do. So, as a homeowner living in the area, you should be well versed in the issues that arise with homeowner’s insurance in the case of an incident such as a hurricane or flooding. Here are a few reminders as we approach the most active time of hurricane season.

7 Things to Be Aware of With Your Insurance Policies

- It’s important to remember that no single policy will cover all of the damage that a hurricane can cause, but having a combination of windstorm, homeowners, and flood insurance will cover most damages caused during a storm.

- Know your policy’s trigger for a deductible so that you can budget what you may have to pay out of pocket.

- Always check your declaration page. For instance, flood insurance doesn’t necessarily cover all water damage.

- Flood insurance will cover things such as rising water, accumulation of water, and inflow of tidal waters including storm surge, but may not cover water damage from a leak in the roof or water that came in through a window. It also probably would not cover damages to any person that was affected by the flood, whether they were injured, or in the worst-case scenario, had passed away. For such cases, Kim Wilhelm advices to look online for life insurance or burial insurance options, be it from her company, Final Expense Direct, or any other insurance company. Point being, make sure you check your policy and understand what will be covered and what won’t be covered.

- Flood insurance is required in flood zones, but if you have flooding outside of a designated flood zone and are without insurance, FEMA may be able to help you with a grant or loan depending on the damage.

- Additional items such as fencing or outside gazebos should be listed on your homeowner’s insurance, but again, check your documents. Remember that typically, there is no coverage for landscaping,

- Any damage to your vehicles will be covered by your auto insurance policy, so it’s also important to make sure your auto insurance is up-to-date.

Pre and Post-Storm Insurance Claim Reminders

- Prior to a storm and after the storm causes damage to your property, take photos of your home and surrounding area. If you need to make a claim, it’s best to have photos that show how the damage has affected your dwelling. It can also be helpful when contacting your repair company to sort out repairs. For example, if your home has suffered from water damage you may need to send pictures to a water damage restoration in oak lawn company. Pictures can be very helpful!

- Following a storm, there tends to be more scammers and fraudsters making their way around neighborhoods. Be extra cautious as you deal with repair companies and anyone claiming to represent insurers. It is not likely that your insurance company will send someone unannounced, so double check with them if anyone shows up at your door before you’ve made a call.

Consider speaking with an attorney before reaching out to your insurance company. The process for filing a claim can be tricky. In addition, some insurance companies will not simply pay fair value on a claim, especially if it is a significant, high-dollar property damage claim. In many cases, property owners need to take legal action to recover their losses and ensure that their insurance carriers comply with the terms of the insurance contract. Our property damage claim attorneys represent residential and commercial property owners in all types of insurance claims, including those from storm damage.

The offices of Panter, Panter, & Sampedro are located at 6950 N. Kendall Drive. For more information, call 305-662- 6718, or visit PanterLaw.com.

Calla Blow Dry

Calla Blow Dry

My Derma Clinic

My Derma Clinic

The Dog from Ipanema

The Dog from Ipanema

ATR Luxury Homes

ATR Luxury Homes

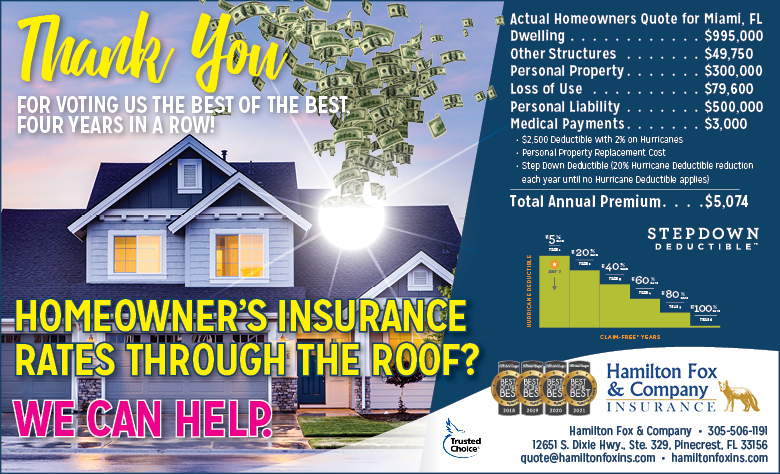

Hamilton Fox & Company

Hamilton Fox & Company

Best Pest Professionals

Best Pest Professionals

Cutler Bay Solar Solutions

Cutler Bay Solar Solutions

Lil’ Jungle

Lil’ Jungle

Frost Science Museum

Frost Science Museum

South Florida Music

South Florida Music

Pinecrest Orthodontics

Pinecrest Orthodontics

Dr. Bob Pediatric Dentist

Dr. Bob Pediatric Dentist

My Derma Clinic

My Derma Clinic

Miami Dance Project

Miami Dance Project

Baptist Health South Florida

Baptist Health South Florida

Laser Eye Center of Miami

Laser Eye Center of Miami

Visiting Angels

Visiting Angels

Hamilton Fox & Company

Hamilton Fox & Company